Flood Risk Assessment for Change of Use

A flood risk assessment for change of use is often needed when you convert a building from one purpose to another — turning offices into flats, a shop into a home, or a barn into a dwelling. Whether one is required depends on the Environment Agency flood zone and, importantly, on whether you're moving to a more vulnerable use. This guide explains when a change of use triggers an FRA, why the type of use matters as much as the location, and what the assessment needs to show.

When does a change of use trigger an FRA?

The same flood zones that govern new buildings apply to changes of use. You'll generally need a flood risk assessment for a change of use in the following situations:

- the building is in Flood Zone 2 or Flood Zone 3 (including the functional floodplain, Zone 3b)

- the site is in Flood Zone 1 but is 1 hectare or larger

- the site is in Flood Zone 1 but lies within a Critical Drainage Area

So far, that mirrors the rules for any development. But change of use has a crucial extra trigger that catches many applicants out, and it's all about vulnerability.

More Vulnerable Use

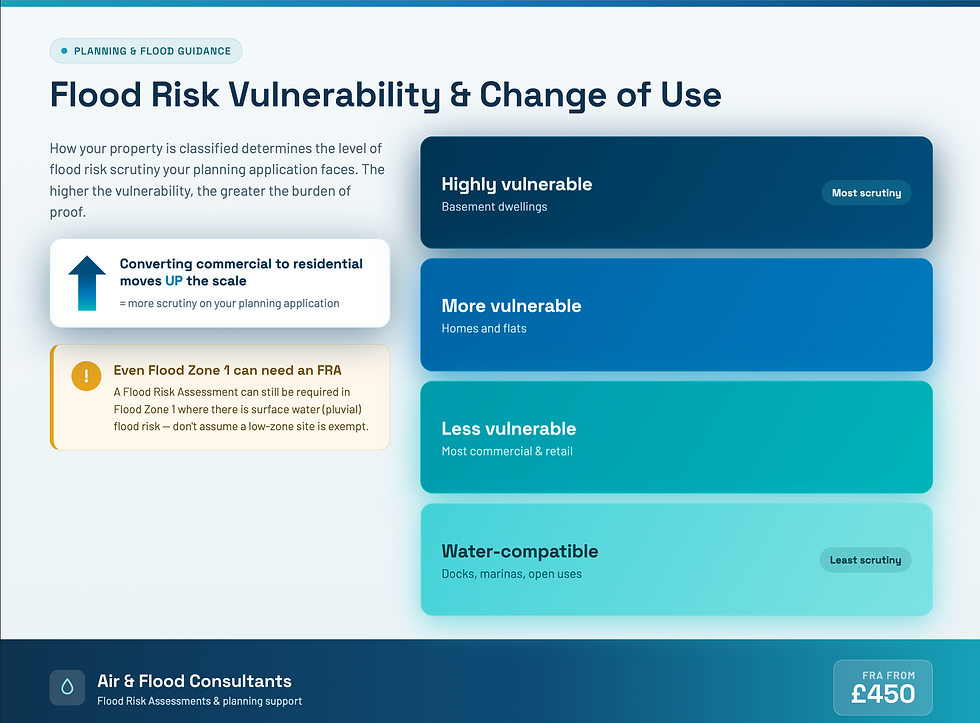

A change to a more vulnerable use class can require an FRA even in Flood Zone 1, where there's a known surface-water flood risk. Converting a commercial unit to residential is the classic example. The walls don't move and the flood zone doesn't change — but the consequences of flooding become far more serious once people are living and sleeping there, so the planning system asks you to look at the risk properly.

If you're not sure which zone applies, our explainer on flood zones 1 vs 2 vs 3 is a useful starting point.

Flood risk vulnerability classification explained

Planning policy sorts land uses into vulnerability categories, set out in the National Planning Practice Guidance. They run from "water-compatible" (things like docks and open space) through "less vulnerable", "more vulnerable", up to "highly vulnerable" (which includes basement dwellings and essential infrastructure).

The category that matters most for conversions is the line between less vulnerable and more vulnerable:

- Most commercial, retail and office uses are classed as less vulnerable.

- Dwelling houses, flats, residential institutions and similar are classed as more vulnerable.

Why does this matter? Because the planning system is far more cautious about putting vulnerable uses — and the people who occupy them — in harm's way. A flooded shop is a clean-up job and an insurance claim. A flooded home, occupied overnight by a family who may not be able to get out, is a risk to life. So when your proposal moves a building up the vulnerability scale, the policy bar rises with it, and an assessment is needed to show the change is safe even where the flood zone itself hasn't changed.

The Sequential Test and Exception Test

For changes of use in flood risk areas, you may also need to engage two policy tests that sit above the FRA itself.

The Sequential Test asks a simple question: are there reasonably available sites at lower flood risk where this development could go instead? It steers development towards lower-risk land. Some changes of use benefit from exceptions to the Sequential Test — for example, certain conversions and changes of use within existing buildings — but you can't assume that; it depends on the proposal and the council's local policy.

The Exception Test comes into play for more vulnerable development in higher-risk zones. To pass, you must show the development delivers wider sustainability benefits and that it will be safe for its lifetime without increasing flood risk elsewhere. The FRA provides the evidence for the second limb.

Getting these tests right early can make or break a conversion. Our guide to the Sequential and Exception Tests explains how they work and when each applies, and a well-prepared flood risk assessment gives the council the safety evidence it needs to apply them.

Common change of use examples

Conversions come in many forms, and the flood risk implications vary with each.

Office to flats

One of the most common conversions, and a textbook jump from less vulnerable to more vulnerable. Even in Flood Zone 1, if there's surface-water risk, expect to need an FRA — and in Zone 2 or 3 it's essential, often alongside the Exception Test.

Shop to dwelling

Converting a high-street shop into a home moves the use up the vulnerability scale. Ground-floor frontages are also prone to surface-water flooding from the street, so finished floor levels and resilience measures usually need careful thought.

Agricultural building to residential

Barn conversions are popular but frequently sit in rural Flood Zone 2 or 3, close to watercourses. An agricultural building is water-compatible or less vulnerable; a dwelling is more vulnerable. That shift, combined with the location, almost always triggers an assessment.

Basement to habitable use

Bringing a basement or cellar into use as living accommodation is the most sensitive change of all. Basement dwellings are classed as highly vulnerable, and in higher-risk zones they may not be acceptable at all. Where they can be considered, safe escape and groundwater are central concerns — see our note on groundwater flood risk.

.webp)

What the assessment covers

A flood risk assessment for a change of use does more than confirm the flood zone. It assesses all sources of flooding affecting the site — rivers, sea, surface water, groundwater and sewers — and judges the risk against the new, often more sensitive, use.

Because the use is changing, the report focuses on whether the proposed occupiers will be safe. That means setting appropriate finished floor levels, recommending flood resistance and resilience measures, and addressing safe access and escape — for residential conversions, a flood evacuation plan may be needed so occupants know what to do if a flood is forecast. The assessment also confirms the change won't increase flood risk to neighbouring properties.

Crucially, it has to look ahead. Planning policy requires development to be safe for its lifetime, which for a new home is taken as 100 years. So the assessment applies the Environment Agency's climate change allowances, testing the conversion against the wetter, higher-risk conditions expected in future rather than just today's flood levels.

Get in Touch

If you're planning a conversion and need to know whether a flood risk assessment is required — and what it will cost — get in touch. We'll review your site, tell you which policy tests apply, and provide a high-quality report that keeps your application moving.

Get in touch to discuss your site and receive a quote.

.webp)